Discover how Uniswap V3 revolutionizes decentralized trading with concentrated liquidity, fee tiers, NFT positions, and Layer 2 support for lower fees.

Uniswap V3 is the third version of the Ethereum ecosystem’s leading decentralized exchange (DEX). Launched in 2021, Uniswap V3 is now a proven standard for capital-efficient, decentralized trading. Its core idea is to enable providers to deploy smarter, targeted liquidity that delivers higher returns with lower capital requirements.

Uniswap V3 is more than an upgrade. It is a fundamental redesign of how automated market makers (AMMs) structure decentralized liquidity. It empowers liquidity providers (LPs) to deploy capital more efficiently. Traders benefit from tighter price execution. Developers gain tools to build faster, cheaper, and smarter financial products.

Uniswap V3 introduces concentrated liquidity, fee tiers, and non-fungible token (NFT)-based positions that give users more control. These changes reshape the user experience and influence the broader decentralized finance (DeFi) ecosystem.

Before diving deeper into the mechanics of Uniswap V3, here are some foundational terms:

Now that we’ve defined some core concepts, let’s look at how Uniswap V3 addresses the inefficiencies of its predecessor.

To understand V3's innovations, it's helpful to revisit where V2 falls short. In Uniswap V2, anyone can become a liquidity provider (LP) by depositing an equal value of two tokens into a pool. These pools follow a constant product formula (x * y = k), and liquidity is distributed evenly across all possible prices by smart contracts.

That sounds fair, but in practice, most capital sits idle. For example, if ETH is trading at $2,000, any liquidity deployed at $1,000 or $4,000 is not used. LPs only earn fees when trades occur within their price range. Since most of the pool sits unused, returns are diluted and impermanent loss risk increases.

In short, two primary limitations of Uniswap V2 are:

One of the most impactful of these changes is concentrated liquidity, which allows LPs to be more strategic about where they allocate capital.

Concentrated liquidity in Uniswap V3 fixes the inefficiencies of V2 by allowing LPs to concentrate their liquidity within specific price ranges. Instead of spreading funds across the entire price curve, LPs can allocate capital around price points where trades are most likely to occur.

In simple terms, V2 sprinkles water across an entire lawn, hoping to nourish one flower. V3 lets you place the sprinkler exactly where it is needed.

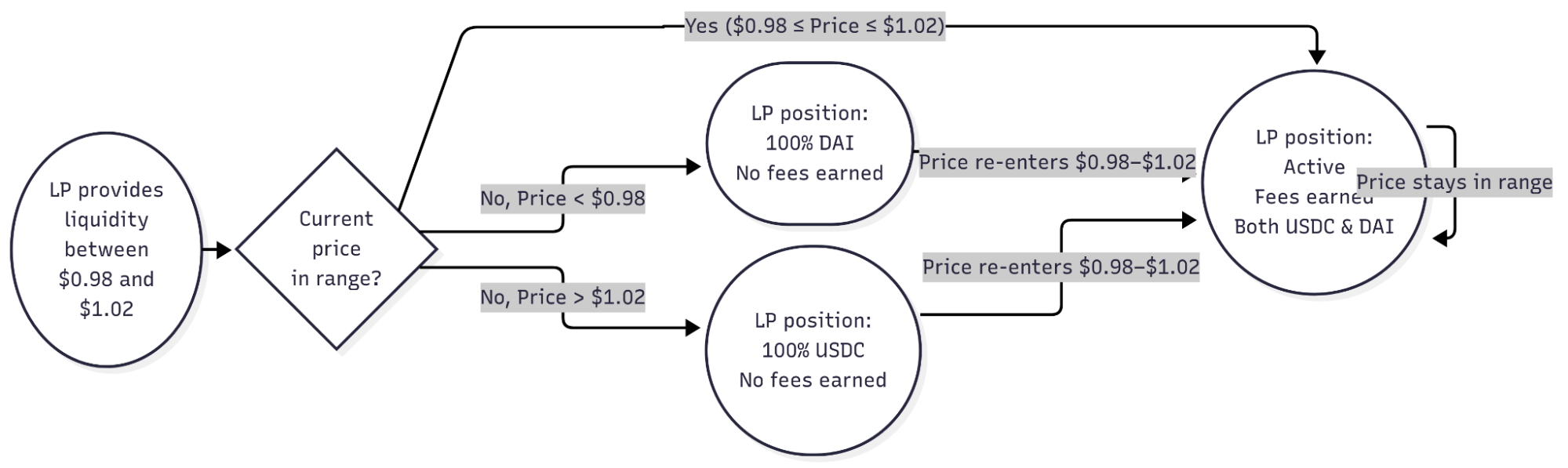

For example, an LP in a DAI/USDC pool might deploy $10,000 between $0.98 and $1.02 (when 1 DAI trades between $0.98 and $1.02 USDC). This narrow range captures nearly all trading activity in a high-volume stablecoin pair, resulting in more trades using that liquidity and thus higher fee income.

This flexibility gives LPs more control over both risk and reward. If the price moves outside their chosen range, their capital remains in the pool but stops earning fees. It becomes fully converted into one of the two tokens, depending on which direction the price moves. Here’s how it works:

The diagram below shows how an LP’s position behaves as the market price moves in and out of the selected range:

This targeted liquidity approach helps LPs have more control over risk exposure. In Uniswap V2, LPs had no way to control their exposure to price divergence. In V3, narrowing the range increases capital efficiency but also amplifies impermanent loss risk. When the price moves outside the selected range, the LP stops earning fees, and its position is fully converted into one of the two assets. This creates greater exposure to price swings compared to V2, where LPs always maintain a mix of both tokens.

Some LPs use automation tools to dynamically rebalance their positions. These tools automatically remove liquidity from positions that are no longer within the current trading price range, and then create new positions with updated price bands. This means closing old positions and opening new ones, which can lead to higher transaction costs.

Others take a more passive approach by choosing wider ranges that require less maintenance. Narrow ranges can yield higher returns on their capital, but demand more frequent monitoring and rebalancing.

In Uniswap V2, every trade pays a fixed 0.30% fee, regardless of asset type or market volatility. Uniswap V3 introduces a more flexible system. LPs can choose between three fee tiers when creating or joining a pool:

This model allows LPs to tailor their strategy. The system encourages market segmentation, helping liquidity naturally concentrate at the most efficient fee levels for each asset pair.

Traders benefit as well. With multiple pools per pair, they can select the pool that offers the best execution for their needs, whether that is the tightest spread or the lowest fee.

Uniswap V3 doesn’t just improve the user-facing features. It introduces under-the-hood upgrades that make it faster, cheaper, and easier to build on.

Uniswap V3 refines the protocol’s core architecture to be more gas-efficient and developer-friendly:

V3’s modular design makes it easier for developers to build DeFi apps on top of Uniswap. TWAP oracles power a range of DeFi protocols, including lending platforms, derivatives, and stablecoins. They require just one on-chain call to compute a time-weighted average price for any period within a predetermined timeframe. This reduces cost, increases reliability, and simplifies integration.

Another major evolution in V3 is how liquidity positions are structured and represented. This has opened up entirely new design possibilities across the DeFi ecosystem.

One of Uniswap V3's most novel features is how it represents LP positions as non-fungible tokens (NFTs). Each user’s individual position becomes a unique ERC-721 token that records the range, liquidity, and fee tier selected. This change opens up new possibilities, but comes with some trade-offs:

This shift from fungible LP tokens to NFTs comes at the cost of reduced composability, but aligns Uniswap V3 with the broader token economy.

Uniswap V3 transforms how liquidity is provided and used. By introducing concentrated liquidity, customizable fees, NFT-based LP positions, more intelligent contract architecture, and enhanced control for LPs, it solves many of V2’s inefficiencies.

This makes Uniswap V3 a foundational protocol shaping how decentralized markets are built and optimized.

Curious how Uniswap V3's innovative architecture works under the hood and how to build with it? Dive deep with Updraft's Uniswap V3 course and unlock the skills to develop cutting-edge DeFi solutions.